TVL SPOT Loading . . . |

|

In this primer we cover the core concepts behind SPOT Protocol using a series of animated diagrams. We'll first describe the outputs of the system at a high level. Then we'll show how this is achieved from the bottom up. For more details ask the community they would love to help!

Here we describe the high level inputs and outputs of the SPOT protocol:

describe $spot ![]()

Commodity monies like gold and bitcoin are durable, decentralized, and inflation resistant, but they are't stable enough for commerce.

SPOT is a low-volatility commodity money. It's durable, decentralized, and inflation resistant, like a commodity money, only far more stable. The SPOT token is created by reorganizing the volatility of its underlying collateral asset (AMPL) into two derivative assets (SPOT, stAMPL):

Holding SPOT and stAMPL together (in the minting ratio) is like holding AMPL because volatility is conserved in the system.

Key Takeaway

SPOT and stAMPL are low and high volatility derivatives of AMPL. More precisely, they are perpetual AMPL tranches. To learn how this works read about AMPL and tranching below.

AMPL is the lowest level building block used in the SPOT protocol. In this section we'll briefly cover AMPL before moving on to tranched AMPL.

describe $ampl

AMPL is a price-stable but supply volatile cryptocurrency that targets the CPI-adjusted dollar. It is used as a unit of account and collateral asset.

The AMPL protocol automatically increases or decreases the quantity of tokens in user wallets — such that the price of AMPL reverts to 1 CPI-adjusted dollar.

In practice, this automatic process of adjusting supply in response to demand takes time to find equilibria.

Key Takeaway

AMPL is a durable, decentralized, unit of account. AMPL's unit of account feature greatly simplifies the creation of on-chain derivatives. Read on to learn how this applies to tranching.

In this section we'll explain fixed-term AMPL tranching.

describe $ampl --tranching

Tranching is the process of reorganizing AMPL's supply volatility into two or more derivative assets with different volatility profiles.

AMPL's volatility, Ai can be separated into senior and junior tranches by tranching:

Holding both [Sri, Jri] is equivalent to holding AMPL because volatility is conserved. After a fixed period of time (defined at the time of tranching) both senior and junior tranches become raw AMPL and rebase normally.

What's Special About This?

AMPL tranching simplifies the process of converting a medium risk asset into two derivative assets: one that is safe and one that's extra risky.

Much of traditional finance works by some variation of this, but the methods used are complex, opaque, and difficult to implement without administrative oversight. AMPL tranching (through Buttonwood Tranche) reduces this to a single operation. Read on to learn about perpetual tranching.

Fixed term tranching, described above, is an extremely powerful financial building block. In fact you can use fixed-term AMPL tranches to create perpetual tranches that reorganize volatility indefinitely.

describe $ampl --tranching --perpetual

Perpetual Tranching is the process of reorganizing AMPL's supply volatility into two or more derivative assets with different volatility profiles —— indefinitely.

AMPL's volatility, A, can be separated into senior and junior tranches perpetually, by bundling multiple fixed-term tranches that are evenly offset by time.

And then systematically rotating maturing tranches out (left), in exchange for fresh tranches in (right):

What's Special About This?

Fixed-term tranching is great for temporarily reorganizing volatility, but fixed-term tranches aren't fungible across vintages because different vintages have experienced different market conditions over time. This makes them less perennially liquid. By bundling multiple vintages into rotating baskets of Sri's and Jri's we can solve for this problem in a simple and highly durable way.

Rotation is the process of withdrawing maturing tranches from SPOT's collateral set and replacing them with fresh tranches. This process is automated (and occurs weekly) through the stAMPL rotation vault. At the time of rotation, the vault::

The newly minted juniors created as a byproduct of tranching, remain in the rotation vault balance (where they are held until they mature into raw AMPL) to be used for future rotations. The diagram below shows the flow of assets.

Referring to the diagram above:

In the case where the AMPL balance in the vault does not cover the entire rollover, it rotates as much as possible. To learn more about the rotation vault in detail, see the rotation vault docs.

Key Takeaway

The rotation vault accepts AMPL from users who want magnified exposure to AMPL's supply changes. For this reason, in addition to holding a basket of corresponding (Jri)'s for every (Sri) in SPOT's colateral set, the rotation vault often holds raw AMPL.

Timely rotations ensure that SPOT's collateral set remains fresh. To incentivize rotations the SPOT protocol utilizes a dynamic rotation fee. This results in the enrichment and debasement of SPOT over long periods of time. In this section we'll cover the basics of how rotation rewards work, explain enrichment / debasement, and link to how this affects SPOT at a high level.

Dynamic Rotation Fee

Broadly the concept of a dynamic rotation fee recognizes there are times when:

This is like the concept of funding rates in traditional markets where sometimes folks pay a fee for going long, sometimes receive a fee for going long, and in a perfectly balanced scenario there are no fees.

In the SPOT system, rotation fees serve to gradually balance the demand for stability and volatility respectively. These fees flow from holders of one asset to the other in a non-extractive way.

Lastly the maximum rate of enrichment (20%) and debasement (10%) are enforced by a simple continuous function. For more detail see the official docs.

Enrichment & Debasement Over Time

To understand how we think about the effect of enrichment and debasement over long time horizons check out: SPOT v2 — Enrichment, debasement, and the cost of stability

Recall that the SPOT protocol works by splitting a medium volatility asset (AMPL) into a high-volatility derivative (stAMPL) and a low-volatility derivative (SPOT).

Additionally:

SPOT & stAMPL exist within bounded volatility ranges

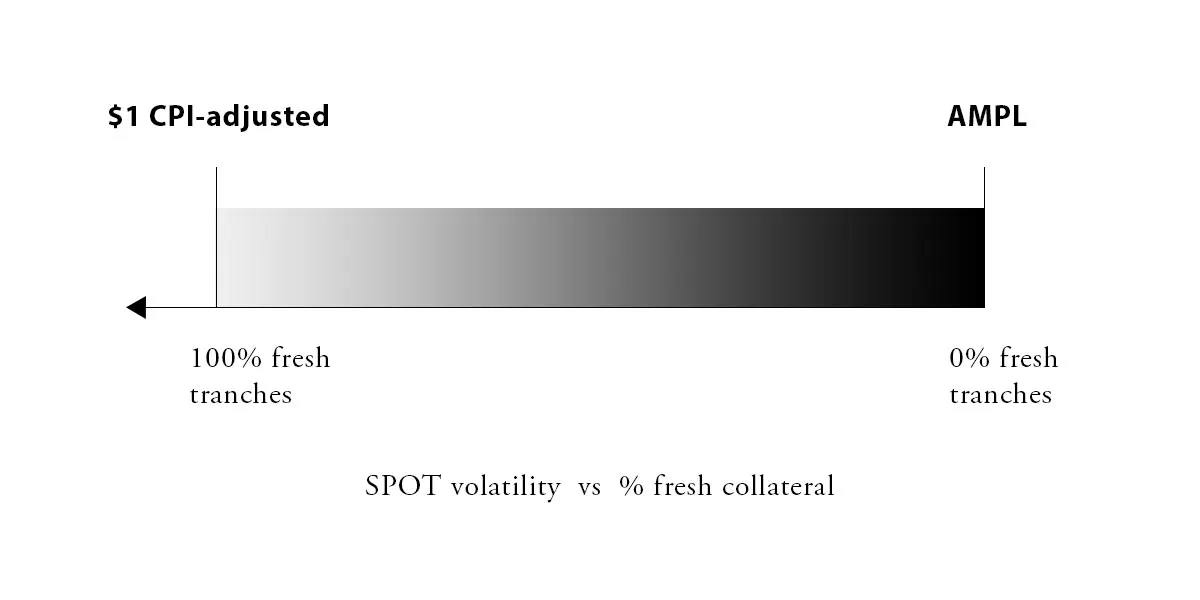

In the typical state, where all the tranches in SPOT’s collateral set are fresh, the token is stable. But in the most extreme scenario, where all the tranches in SPOT’s collateral set have matured, SPOT is precisely as volatile as AMPL.

SPOT’s minimum volatility is that of the 2019 CPI-adjusted dollar (left) when 100% of the tranches in its collateral set are fresh. And SPOT's maximum volatiliy is equivalent to AMPL’s (right) when 0% of the tranches in its collateral set are fresh.

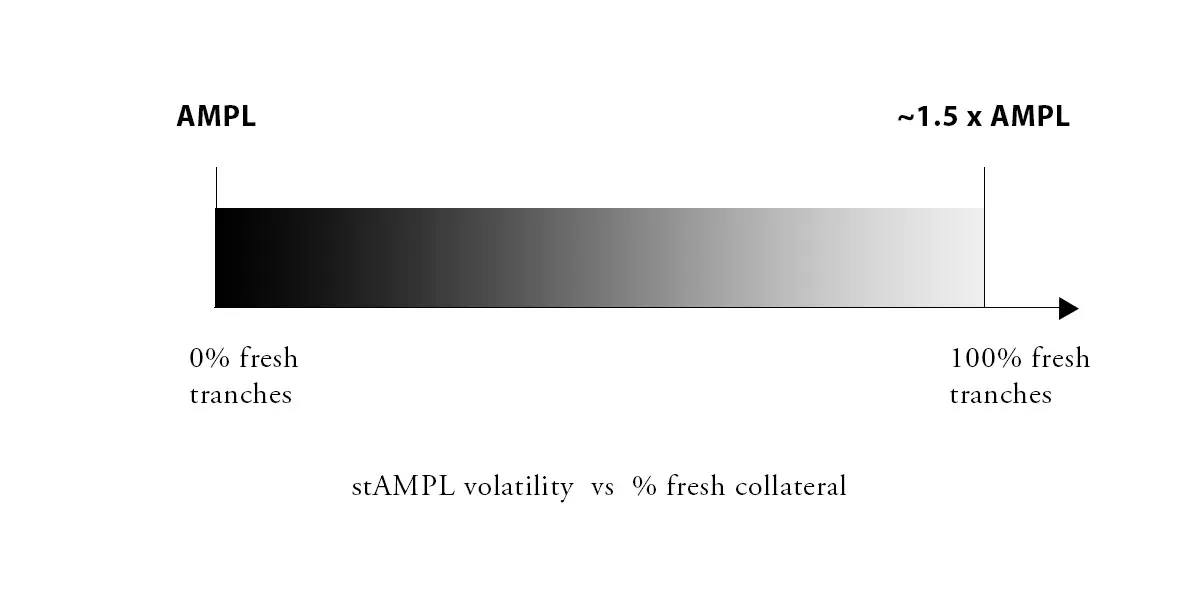

Similarly, when all the tranches in stAMPL’s collateral set are fresh, the stAMPL token is ~1.5x as volatile as AMPL. And when all the tranches in stAMPL’s collateral are mature, stAMPL is precisely as volatile as AMPL.

stAMPL’s volatility has a min equivalent to AMPL’s (left) when 0% of the tranches in its collateral set are fresh. And a max volatility of about ~1.5 x AMPL’s (right) when 100% of the tranches in its collateral set are fresh.

The system can go from being collateralized entirely by fresh tranches, to all mature tranches, and vice-versa. Just as tranched AMPL can mature into raw AMPL when rotation balances are insufficient, raw AMPL can be rotated out for tranched AMPL whenever rotation balances become sufficient.

There Are No Catastrophic Breaking Conditions

There are no pegs. And for every quantum of stability in the SPOT system there is a transparent amount of volatility that affords it. Nothing is obfuscated, hand-waived, or ignored. All risk in the system can be seen and priced. Under extreme market conditions SPOT simply gets temporarily more volatile. For expanded commentary on this see: The SPOT Flatcoin — A Low Volatility Derivative.

The Marginal Utility of SPOT

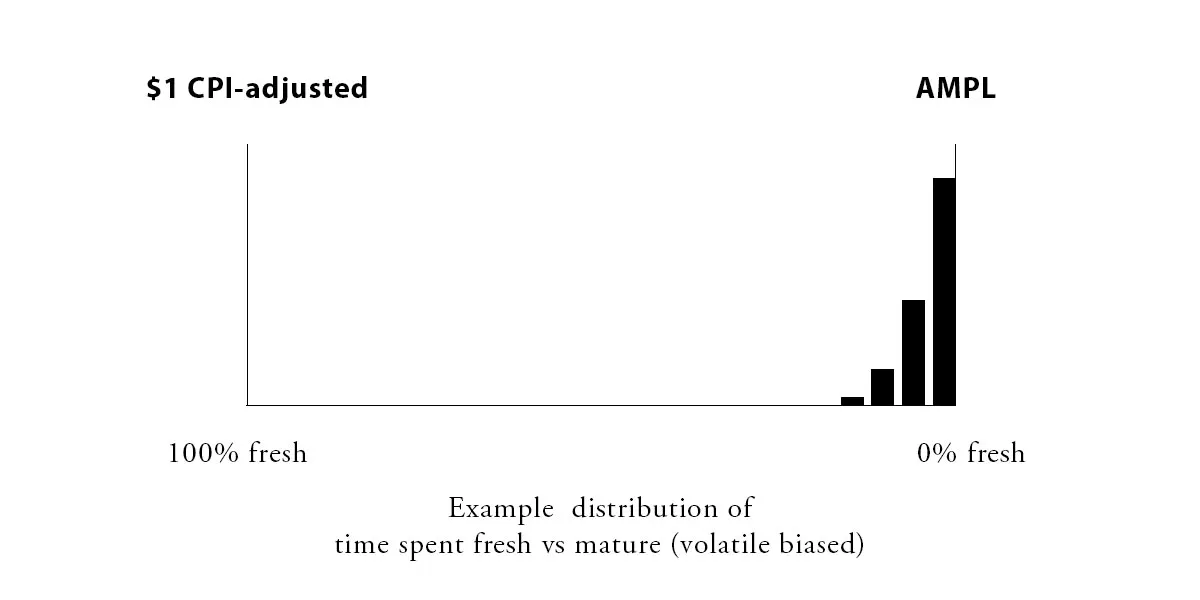

The marginal utility of SPOT will be determined by its distribution of time spent: near the volatility levels of the CPI-adjusted dollar vs near the volatility levels of AMPL. In the likely scenario where most of SPOT’s time is spent near the CPI-dollar multiple, it is sufficiently low in volatility to be used as a peer-to-peer digital cash and refuge from inflation.

In the unlikely scenario that almost no time is spent near the CPI-dollar multiple, it’s a commodity-money with no non-monetary utility, much as Bitcoin is. And can be used as a different sort of refuge from inflation (ie: the way equities and other investment assets can be thought of as a refuge from inflation).

And you can imagine any number of time distribution scenarios in between the two described above. For commentary on how we expect SPOT to perform over long time horizons see: SPOT v2 — The cost of stability

SPOT supply is freely determined by market demand for minting and redeeming. However, there are natural incentives to mint and redeem SPOT based on the market value of AMPL.

Liquidation-market based systems: rely on continuous demand for margin-leverage on collateral in order to maintain a fixed circulating supply. This makes them very difficult to scale. In such systems, minters lock up capital to create the stablecoin. They constantly pay interest, monitor the position and top up with more capital if they are underwater to avoid losing their position through liquidations.

In the SPOT system, arbitrageurs don't have the burden of managing an open CDP and paying an ongoing fee while worrying about getting liquidated. We've mentioned previously that:

For this reason, the floor of SPOT's circulating supply is determined by the base-rate demand for holding AMPL rather than demand for amplified volatility. Above this floor of base rate demand, the circulating supply of SPOT can increase or decrease based on relative demand for stability (SPOT) or amplified volatility (stAMPL) respectively.

Lastly, in the case of SPOT demand for stability propagates into demand for AMPL through minting / redeeming arbitrage whereas in delta neutral systems like Ethena, demand for stability does not create demand for leveraged ETH.

For more on this see: About Scalability

Some of these have been linked to already above but we recommend the following:

Big Picture

Technical Details